Revenue, 2025

$0.9Bn

Forecast, 2035

$14.0Bn

CAGR, 2025-2035

31.6%

Report Coverage

Global

Market Size and Forecast

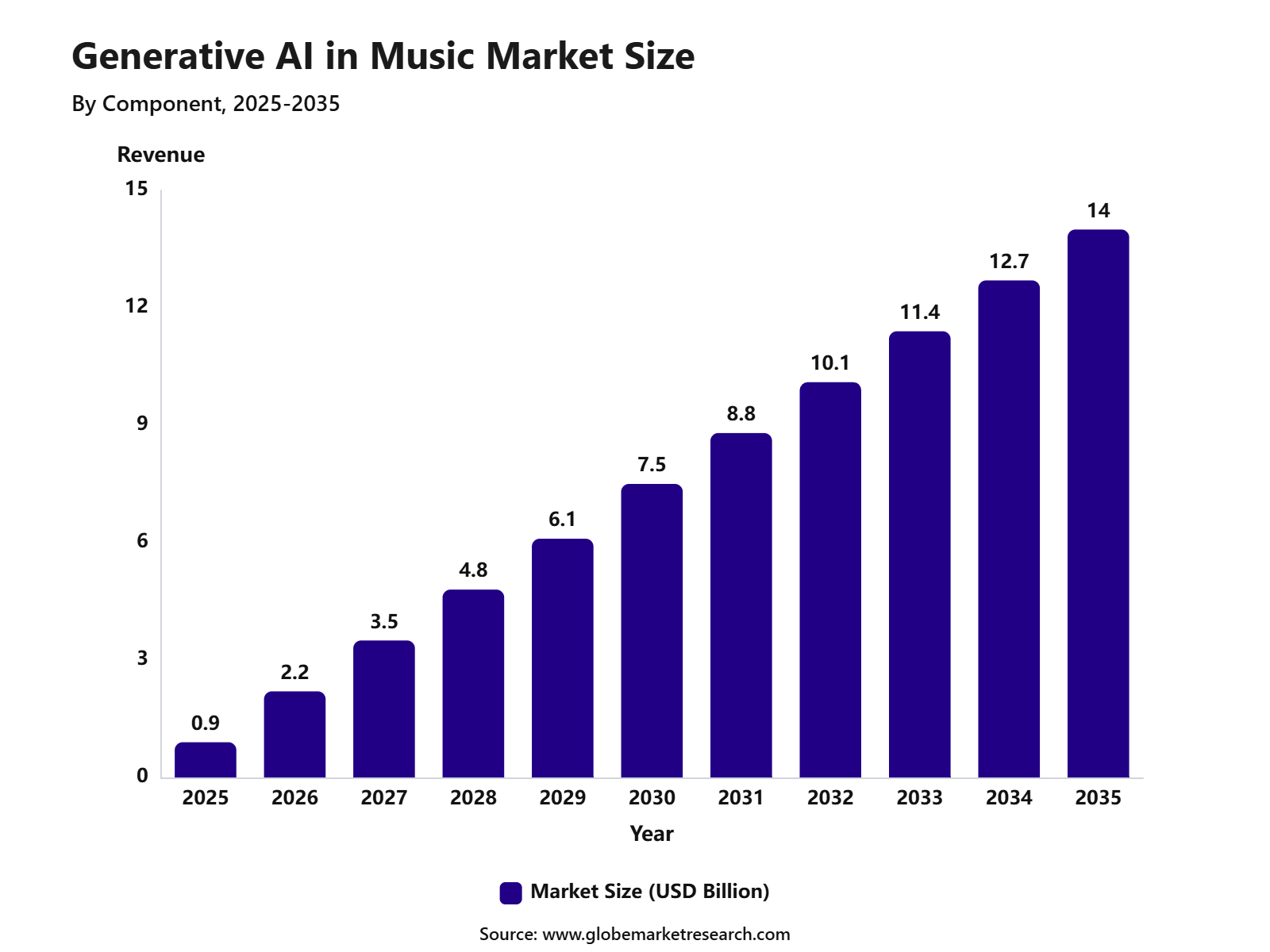

The Global Generative AI in Music Market was valued at USD 0.9 billion in 2025 and is projected to reach USD 14.0 billion by 2035, reflecting a robust compound annual growth rate of 31.6%. North America led the market in 2025 with a 38.6% share, supported by the presence of advanced music production infrastructure, high adoption of AI-driven music software, and a strong ecosystem of content creators and streaming platforms. The region’s leadership is further reinforced by significant investment in AI research, technological innovation, and early adoption of generative AI solutions in media and entertainment.

The growth of generative AI in music has been supported by multiple factors. First, investments in computational infrastructure and more sophisticated AI models have accelerated the capability and quality of music generation tools. Second, there is increasing demand for personalized audio experiences among listeners, prompting streaming services to integrate AI-driven music curation and generation into their offerings. Third, artists, producers, and independent creators are adopting AI tools to augment their workflows, reduce production time, and lower creative barriers. These drivers collectively contribute to a rapidly expanding market landscape.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFTop Market Takeaways

Solutions led the market by component with 69.2% share, supported by widespread adoption of AI platforms, music generation tools, and workflow integration for composers and producers.

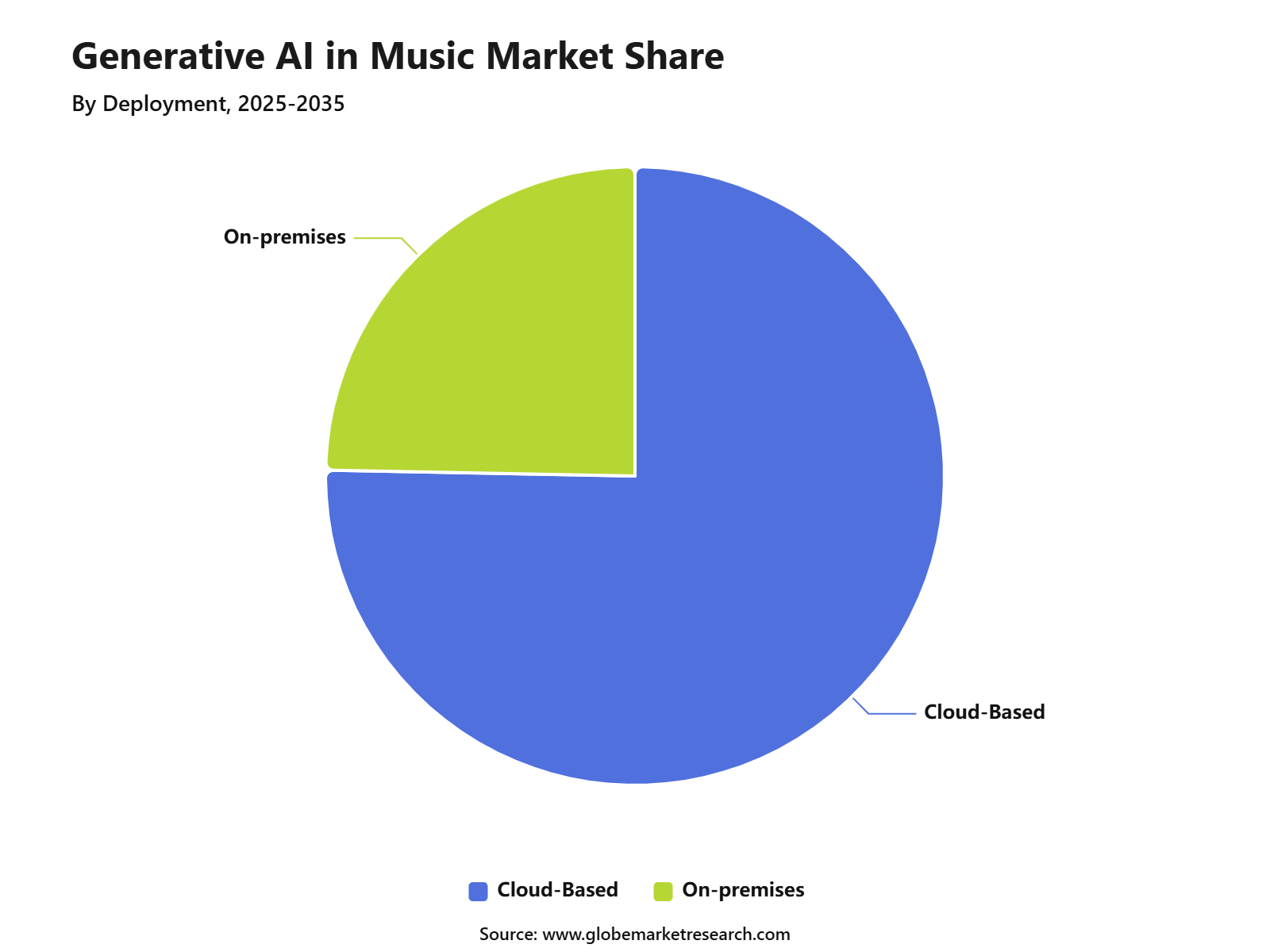

Cloud-based deployment dominated with 75.3% share, driven by scalability, remote collaboration, and easier access to AI-powered music tools.

Music composition and generation accounted for 29.6% share by application, supported by growing demand for automated music creation, style transfer, and personalized soundtracks.

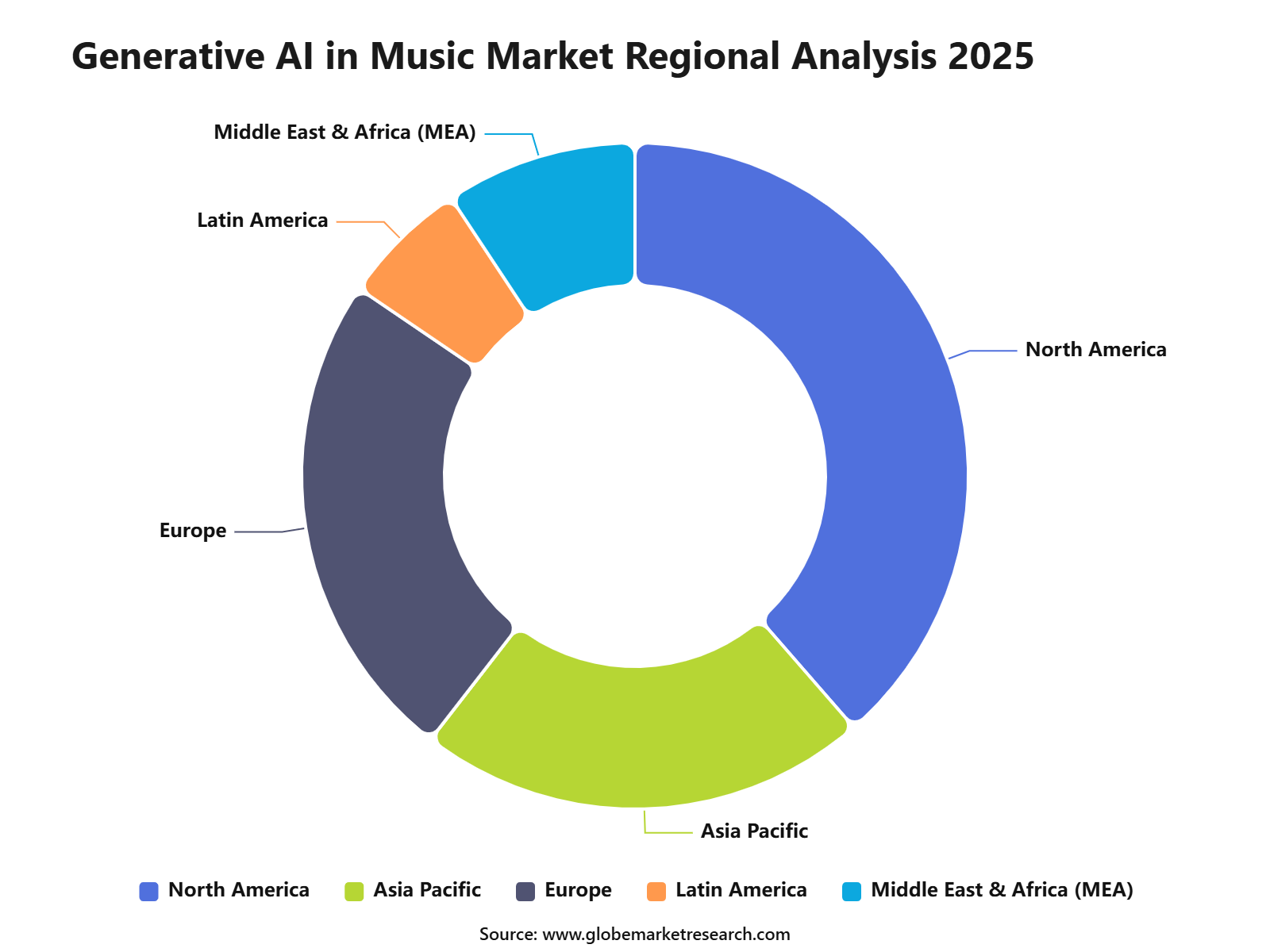

North America held 38.6% share of the market, supported by early adoption of AI technologies, strong music production infrastructure, and active digital content consumption.

Market Overview

Demand is rising from music creators who want tools that support idea generation, demo creation, and faster production workflows. Songwriters can use AI to test lyrics, chord progressions, melodies, and vocal styles before entering a full studio process. Producers can use AI to build rough versions of tracks, separate vocals and instruments, or improve sound quality. This demand is especially strong among independent artists who need professional results with limited budgets.

Investment opportunities are growing in AI music creation platforms, production tools, licensing systems, and rights protection technologies. The funding environment also shows strong investor interest, as AI music company Suno raised more than USD 400 million in June 2026. The funding round valued the company at USD 5.4 billion, which reflects rising confidence in AI-powered music creation tools. This indicates that investors are viewing AI music as a serious part of the future creator economy.

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 0.9 Bn |

Forecast Revenue (2035) | USD 14.0 Bn |

CAGR (2025-2035) | 31.6% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | Market Surveys, Trade Analysis, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends |

Segments Covered | By Component (Solutions, Services), By Deployment (Cloud-based, On-premises), By Application (Composition and Music Generation, Performance Enhancement and Virtual Collaboration, Personalized Music Recommendations, Music Production and Remixing, Music Transcription and Analysis, Other Applications) |

Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Aiva Technologies SARL, Boomy Corporation, Ecrett Music, Google LLC, International Business Machines Corporation, LANDR, Meta, Microsoft, OpenAI, Stability AI, Other |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Generative AI Music Industry Statistics

The recorded music industry remains strongly digital. In 2025, global recorded music revenue grew 6.4% to USD 31.7 billion, with streaming accounting for around 70% of global music income.

Generative AI is projected to contribute between $2.6 trillion and $4.4 trillion annually to the global economy by 2030.

The WIPO recommends clarifying AI authorship and copyright ownership by 2025, with 80% of countries supporting updated guidelines.

60% of musicians currently incorporate some form of AI into their creative workflow.

Approximately 35% of artists use AI tools for mastering their tracks.

Over 1 million AI-generated tracks are uploaded to streaming platforms each month.

20% of music producers utilize AI for lyric generation and songwriting support.

47% of independent artists believe AI helps them complete songs more quickly.

There are more than 500 active AI music generation platforms publicly available.

Paid streaming is the main commercial base for music platforms. Paid subscription streaming grew 8.8% in 2025 and reached 837 million paid subscription accounts worldwide.

By Component

In 2025, Solutions accounted for 69.2% of the Generative AI in Music Market, as creators, production teams, advertisers, and media companies prefer ready-to-use platforms over standalone services. These solutions support music composition, melody creation, lyric assistance, sound design, voice synthesis, audio enhancement, and remixing. Their dominance can be attributed to ease of use, faster production cycles, and the ability to support both skilled musicians and non-technical users.

The growth of the solutions segment is also supported by the rising need for controlled and scalable music creation tools. Users are increasingly looking for platforms that can generate background scores, short-form music, demo tracks, and customized audio for digital content. However, solution providers are also being pushed to improve transparency, consent management, and artist protection. This makes trusted, rights-aware software solutions more important for long-term adoption.

By Deployment

In 2025, Cloud-based deployment held the largest share at 75.3%, mainly because generative AI music tools require high computing power for training, inference, storage, and audio rendering. Cloud platforms allow users to access advanced music generation tools without investing in costly local hardware. This model is especially useful for creators, studios, agencies, and app developers that need quick access to AI models through browsers, APIs, and subscription platforms.

The cloud model also supports real-time updates, collaboration, batch music generation, and flexible scaling. Music creators can produce multiple versions of tracks, test different moods, and manage audio files from any connected device. For enterprises, cloud deployment offers better integration with content platforms, licensing systems, and workflow tools. As a result, cloud-based platforms are expected to remain the preferred delivery model for commercial AI music tools.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Application

In 2025, Composition and music generation represented the leading application segment with 29.6% share, as this is the most direct and widely used function of generative AI in music. These tools help users create melodies, beats, chord progressions, lyrics, instrumental tracks, and full music samples from text or audio prompts. The segment is gaining traction because it reduces the time required to move from idea to usable sound.

Demand is also rising from content creators, game developers, social media producers, advertisers, and independent artists who need original audio at lower cost and faster speed. AI-generated composition is not replacing human creativity, but it is becoming a useful support tool during ideation, experimentation, and early-stage production. The strongest adoption is seen where AI helps users generate drafts, test styles, and personalize music for specific content needs.

Region Analysis

In 2025, North America held the dominant share of 38.6% in the Generative AI in Music Market, supported by a strong base of AI developers, digital music platforms, investors, cloud infrastructure providers, and entertainment companies. The region has been an early adopter of AI-powered music tools across creator platforms, media production, advertising, gaming, and streaming-related workflows. High digital content consumption further supports demand for faster and more flexible music creation.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe region also plays a major role in shaping the legal and commercial direction of AI music. Copyright, artist consent, voice protection, and licensing are becoming central issues for platform developers and music rights owners. This has encouraged companies to build safer tools with clearer policies, watermarking, licensing controls, and artist-protection features. Due to this mix of innovation, investment, and regulatory attention, North America remains the key region for market development.

Regional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +8.2% | U.S. and Canada | Drives early adoption and revenue share. |

Europe creative adoption | +6.7% | UK, Germany, France, Italy | Supports music production integration. |

Asia Pacific rapid expansion | +7.0% | Japan, China, South Korea, India | Boosts AI music tool usage. |

Latin America emerging adoption | +5.4% | Brazil, Mexico, Argentina, Chile | Provides new consumer base. |

Middle East and Africa growth potential | +4.9% | UAE, Saudi Arabia, South Africa | Opens early-stage market opportunity. |

Key Market Segments

By Component

Solutions

Services

By Deployment

Cloud-based

On-premises

By Application

Composition and Music Generation

Performance Enhancement and Virtual Collaboration

Personalized Music Recommendations

Music Production and Remixing

Music Transcription and Analysis

Other Applications

By Region

North America

Europe

Asia Pacific

Latin America

Middle East & Africa

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising adoption of AI in music composition | +8.2% | North America, Europe, Asia Pacific | Expands automated music creation demand. |

Growth of streaming platforms and digital music | +7.6% | U.S., China, Europe, India | Drives AI-generated content consumption. |

Increasing demand for personalized music experiences | +7.0% | Global | Enhances user engagement and retention. |

Rising investment in AI-driven music startups | +6.5% | U.S., Europe, China | Supports innovation and new tools. |

Integration of AI in video games, film, and advertising | +6.3% | Global | Expands commercial application of generative music. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High cost of advanced AI music solutions | -3.4% | Global | Limits adoption among smaller studios. |

Limited AI-trained musicians | -3.0% | U.S., Europe, Asia Pacific | Slows creative workflow integration. |

Copyright and intellectual property concerns | -2.7% | Global | Raises legal and licensing challenges. |

Skepticism toward AI-generated content | -2.5% | North America, Europe, Japan | Slows consumer acceptance. |

Integration complexity with existing DAWs | -2.1% | Global | Delays workflow adoption. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Expansion in AI-assisted music composition tools | +7.8% | U.S., Europe, Japan, China | Supports professional and amateur adoption. |

Growth of AI-generated music for commercials | +7.1% | North America, Europe, Asia Pacific | Creates new revenue streams. |

Rising interest in royalty-free AI music libraries | +6.7% | Global | Enhances licensing flexibility. |

Integration with metaverse and immersive platforms | +6.3% | North America, Asia Pacific | Expands experiential music use. |

Increasing demand for multilingual and cultural music generation | +6.0% | U.S., China, India, Europe | Supports globalized content creation. |

Challenges Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Ethical concerns over AI creativity | -3.2% | Global | May slow acceptance by artists and industry. |

Quality limitations of AI compositions | -2.8% | Global | Affects professional adoption. |

Rapid evolution of AI models | -2.5% | Global | Requires continuous investment. |

Dependence on high-performance computing | -2.3% | North America, Europe, Asia Pacific | Raises operational costs. |

Limited standardization of AI-generated music formats | -2.0% | Global | Creates workflow integration issues. |

Recent Developments

June 2026 – Suno raised USD 400 million in a Series D funding round at a USD 5.4 billion valuation. This investment is intended to accelerate expansion of its generative AI music tools and improve creative capabilities amid continued legal scrutiny over copyrighted training data. Institutional backers include Bond Capital, IVP, Forerunner, and Union Square Ventures, reflecting strong investor confidence in AI music innovation.

February 2026 – Google acquired ProducerAI, a generative AI music startup, integrating its team and technology into Google Labs. The acquisition strengthens Google’s AI‑driven music creation stack and aligns with the company’s broader creative AI strategy, including advanced generative models for music generation in mobile and cloud platforms.

January 2026 – BeatStars acquired ethical generative music startup Lemonaide AI to integrate AI‑assisted creation tools into its platform. This deal, following a prior strategic alliance, aims to establish creator‑centric AI features and deepen AI capabilities for music producers and independent artists, though financial terms were not disclosed.

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Aiva Technologies SARL

Boomy Corporation

Ecrett Music

Google LLC

International Business Machines Corporation

LANDR

Meta

Microsoft

Stability AI

OpenAI

Others Key Players

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Manoj H. brings more than 7 years of professional experience in market research, business intelligence, and industry-focused analysis. His research background covers detailed market assessment, competitive benchmarking, consumer and industry trend tracking, and strategic opportunity evaluation across multiple global sectors. Over the years, Manoj has worked on a wide range of research assignments involving market estimation, company analysis, value chain assessment, regional outlook, and growth opportunity mapping. His expertise lies in converting complex business data into clear, useful, and decision-ready insights for companies, investors, consultants, and industry stakeholders.

Pratiksha is market research analyst with strong experience in industry research, market forecasting, and competitive analysis. She specializes in identifying market trends, evaluating growth opportunities, and preparing data-driven insights across global industries. Her work supports businesses in understanding market dynamics, customer demand, regional opportunities, and strategic investment areas.

Frequently Asked Questions

Related Reports

More in Information and Technology

Answer Engine Optimization (AEO) Market Size to Reach USD 91.3 Billion By 2035

Global Answer Engine Optimization (AEO) Market Size, Go-to-Market and Sales Strategy Analysis By Offering (Software / Platforms, Services), By Deployment Mode (Cloud-based, On-premises), By Organization Size (SMEs, Large Enterprises), By Channel Type (Search Engines, AI Chat Interfaces, Voice Search), By Functionality (Query & Intent Optimization, NLP / Semantic Optimization, Analytics & Performance Tracking), By End-Use Industry (BFSI, Retail & E-commerce, Healthcare, IT & Telecom, Media & Entertainment, Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Agentic AI Travel Booking Platforms Market Size to Reach USD 31.4 Billion By 2035

Global Agentic AI Travel Booking Platforms Market Size, Go-to-Market and Sales Strategy Analysis By Technology (AI Trip Planning Agents, Machine-Readable Rate APIs, Loyalty Integration, Autonomous Price Comparison and Others), By User Type (Business Travelers, Group Bookings, Leisure Travelers and Others), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

5G RAN Market Size to hit USD 108.5 billion by 2035

Global 5G RAN Market Size, Go-to-Market and Sales Strategy Analysis By Component (Hardware, Software, Services), By Architecture Type (Traditional RAN, Open RAN), By Deployment (Public Networks, Private Networks), By End Use (Telecom Operators, Enterprise and Industrial Users), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035

Online Dating Market Size to hit USD 29.5 Bn by 2035

Global Online Dating Market Size, Go-to-Market Strategy Analysis By Type (Paying Online Dating, Non-Paying Online Dating), By Revenue Model (Subscription, Advertising-Supported, Other Model), By Platform (Web Portals, Applications), By Age Group (Adult, Baby Boomer, Generation X, Generation Z, Millennials), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts By 2025-2035