Revenue, 2025

$279.8 bn

Forecast, 2035

$1,255.8 bn

CAGR, 2025-2035

16.2%

Report Coverage

Global

Market Size and Forecast

2025

$279.8 bn

2035

$1,255.8 bn

CAGR

16.2%

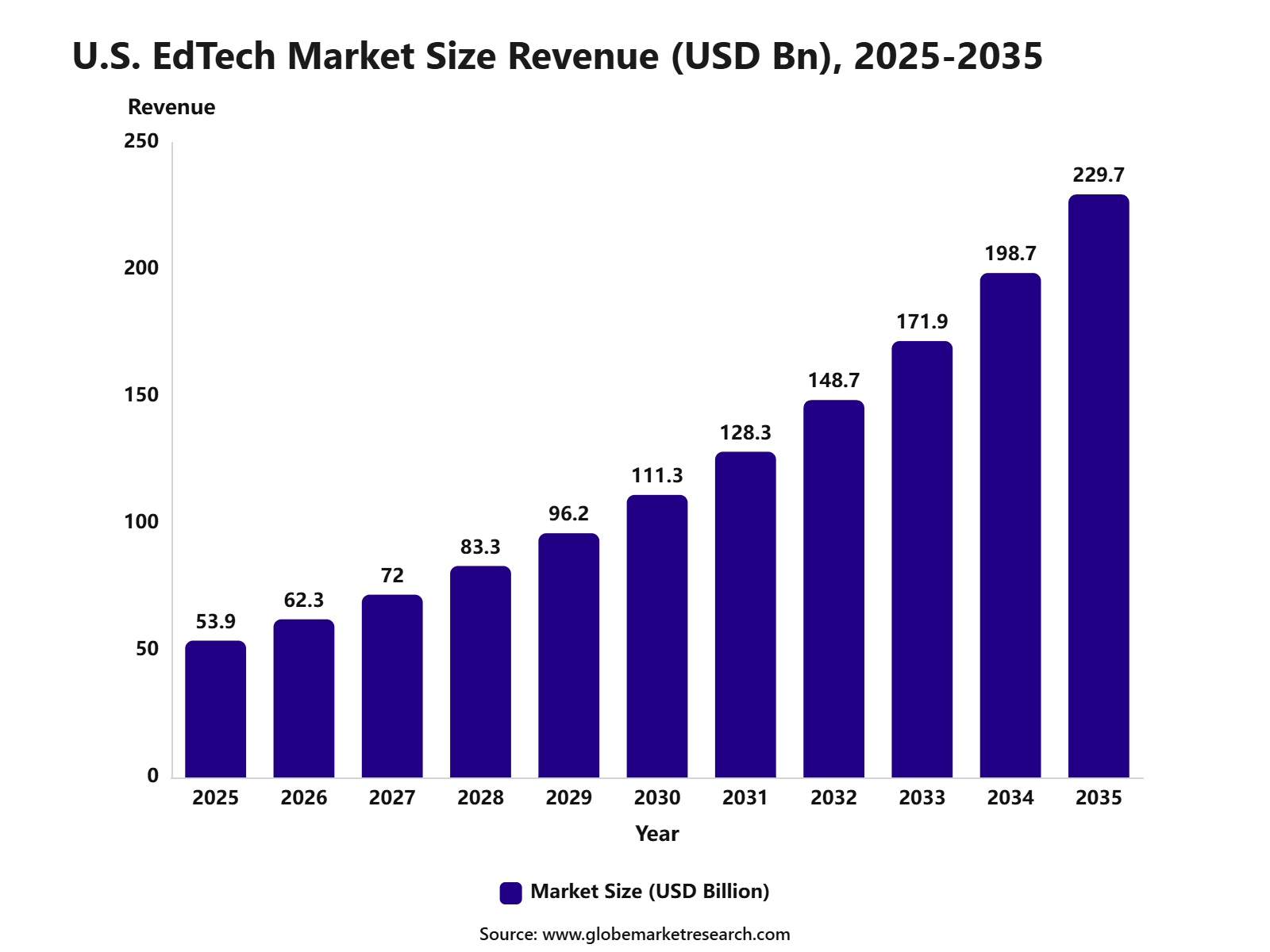

The global EdTech market was valued at USD 279.8 billion in 2025 and is projected to reach USD 1,255.8 billion by 2035, growing at a CAGR of 16.2% during the forecast period. North America held a leading position in the EdTech market, accounting for 39.8% share in 2025. The U.S. market was valued at USD 53.9 billion in 2025 and is expected to grow at a CAGR of 15.6%, supported by strong digital infrastructure, high spending on education technology, and growing adoption of personalized learning tools.

The growth of the EdTech market is being supported by rising internet access, wider smartphone use, demand for flexible learning, and the growing need for digital skills. In 2025, around 6 billion people, or nearly three-quarters of the global population, were using the internet, which created a larger base for online learning platforms and digital education services.

The digital divide continues to shape demand for affordable and low-bandwidth learning solutions. ITU reported that 2.2 billion people remained offline in 2025, while UNICEF and ITU earlier found that 2.2 billion children and young people aged 25 years or below did not have internet access at home, creating strong long-term demand for inclusive digital education infrastructure.

Key Insight Summary

By sector, K-12 leads the market with around 59.1% share, driven by wider adoption of digital learning tools in schools.

By type, hardware accounts for 41.9% , supported by rising demand for tablets, laptops, smartboards, and classroom devices.

By deployment mode, on-premise solutions dominate with 72.3% share, as many institutions prefer direct control over data and systems.

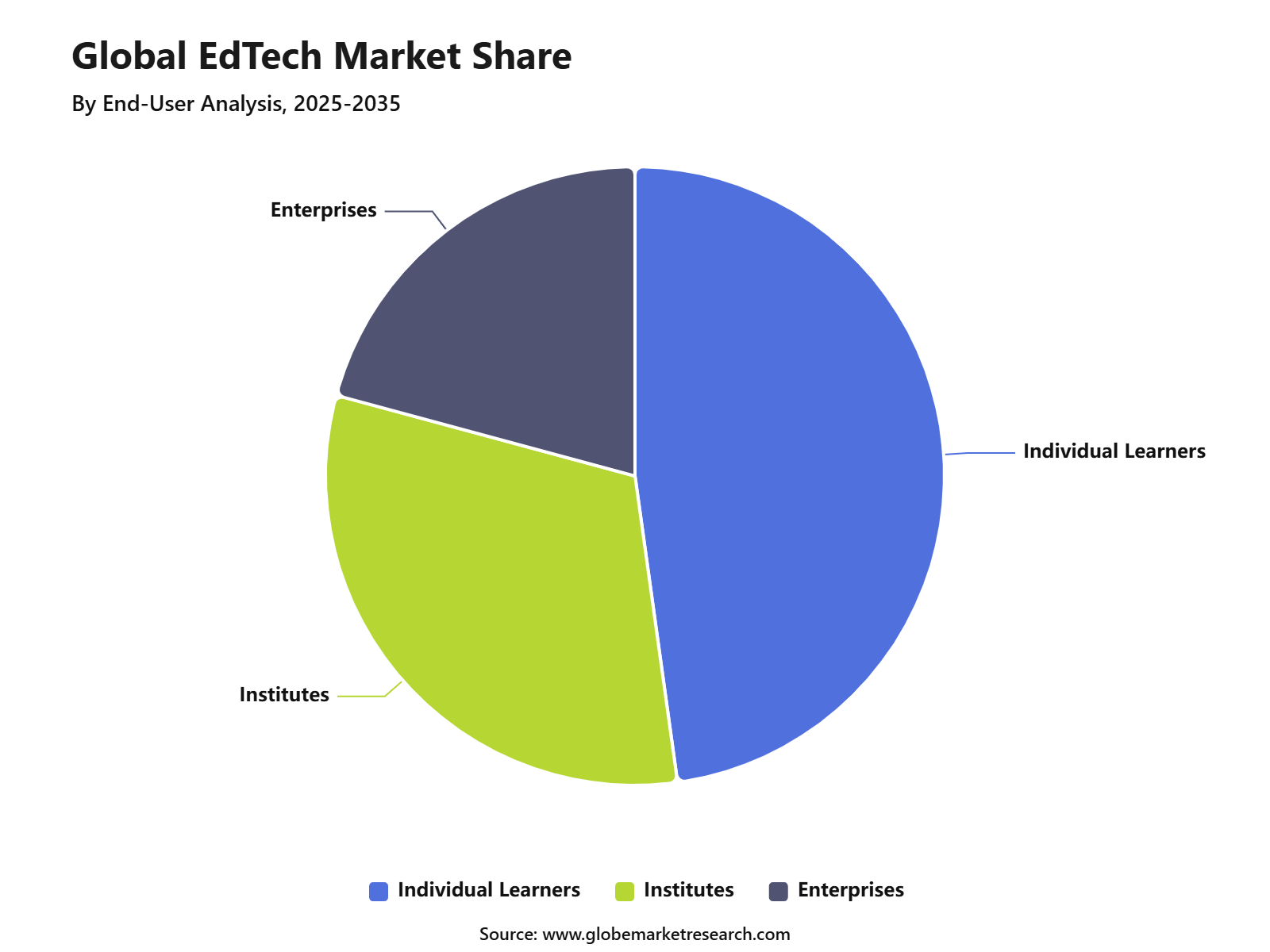

By end-user, individual learners lead the market with around 47.8% share, supported by growing use of online courses, mobile learning apps, and self-paced education platforms.

North America is expected to hold a strong position in the EdTech market, supported by 39.8% growth. The U.S. market is valued at USD 53.9 billion and is projected to expand at a CAGR of 15.6% .

Role of Agentic AI

Agentic AI is gaining importance in the EdTech market because it can act as an active learning assistant rather than a simple response-based tool. It can plan lessons, suggest learning paths, generate practice questions, track progress, and recommend the next step based on student performance.

The adoption of AI in education is increasing as students and institutions use digital tools for learning support. In the UK, the share of students using generative AI tools for assessment-related work increased from 53% in 2024 to 88% in 2025, showing a sharp rise in AI-assisted academic activity. This creates a strong base for agentic AI tools that can support tutoring, revision, writing guidance, and study planning.

Agentic AI can support teachers by reducing repetitive tasks such as lesson planning, quiz creation, feedback preparation, and progress monitoring. OECD data showed that in 2024, AI was used regularly in classrooms by 8% of primary school students, 30% of lower-secondary students, 50% of general upper-secondary students, and 42% of vocational learners. This shows that AI-enabled learning tools are moving into regular education use across different student groups.

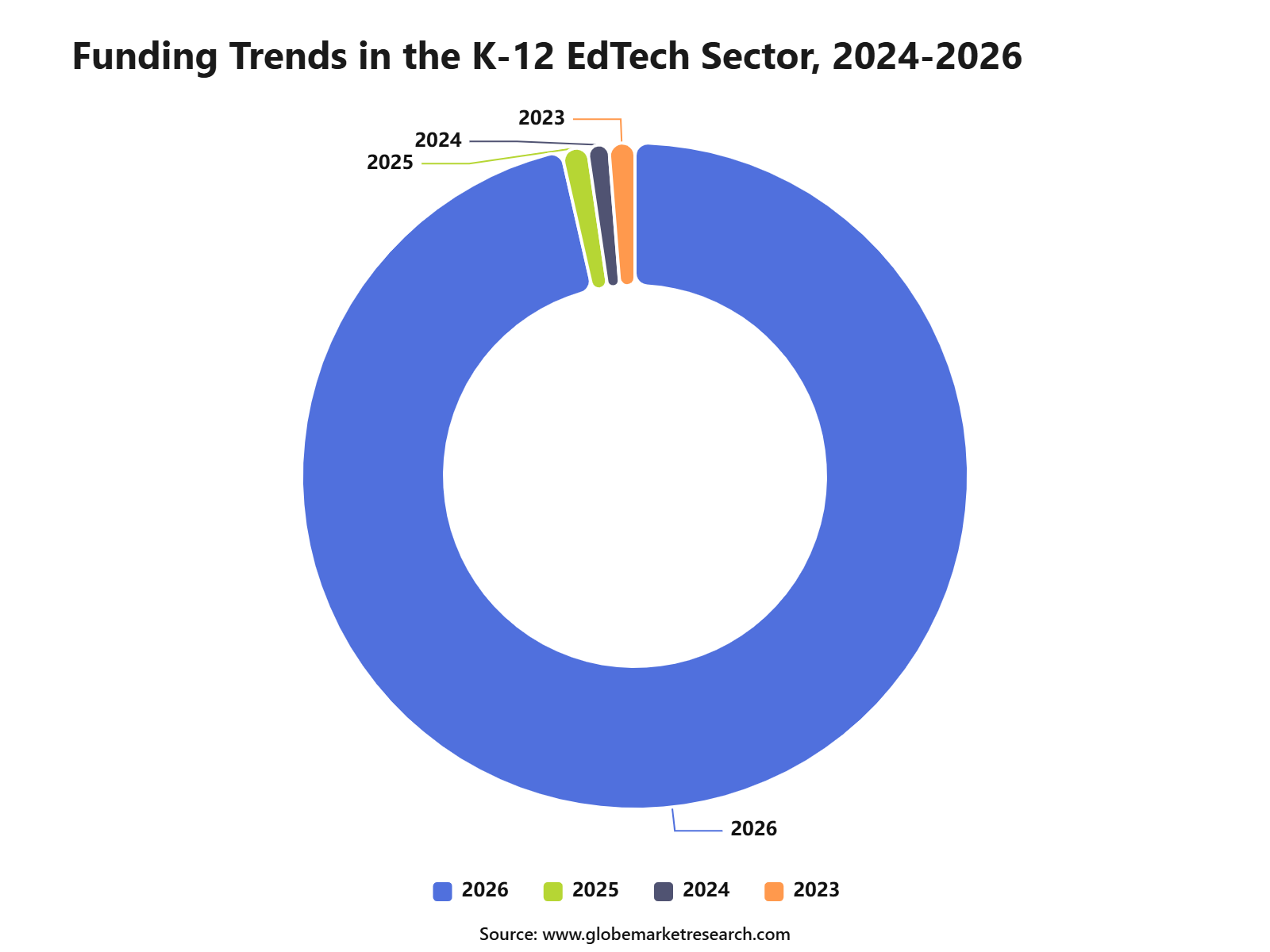

Funding Trends

The K-12 EdTech sector has attracted strong investor interest over the past decade, supported by the rapid adoption of digital classrooms, online tutoring, learning platforms, and school management technologies. Based on Tracxn data, the sector received more than USD 40 billion in total funding over the last 10 years, with investment activity reaching its highest level in 2020, when funding exceeded USD 12.3 billion.

Funding activity has moderated after the pandemic-led investment surge, but capital inflow continues across AI learning platforms, digital curriculum tools, assessment solutions, and school-focused software. In 2026 till date, the K-12 EdTech sector has raised around USD 122 million, showing selective investor interest in scalable, outcome-driven, and technology-enabled education models.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

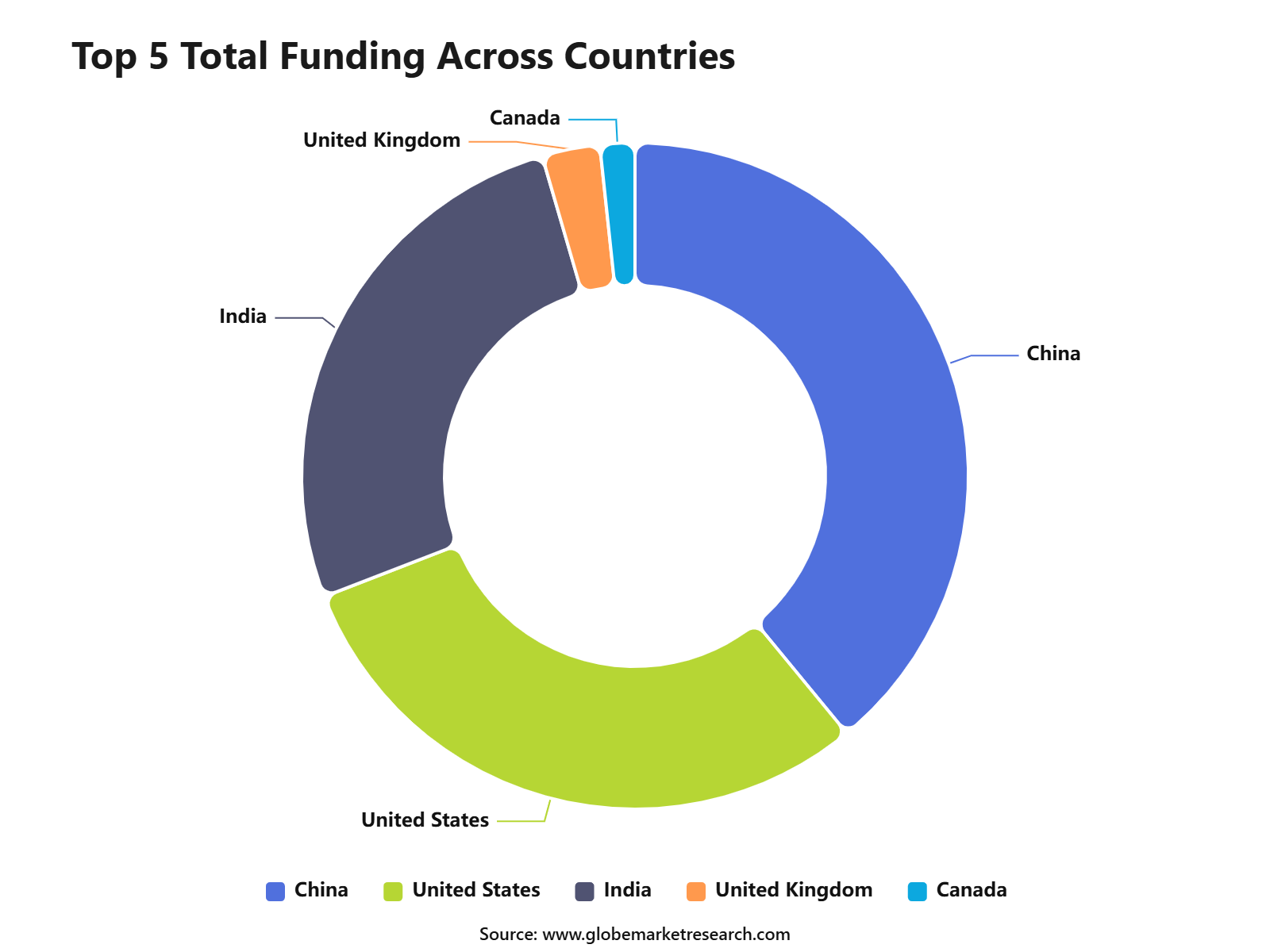

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFTotal Funding Across Countries

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRecent Funding

Company | Round Raised | Amount Raised | Investors |

|---|---|---|---|

Qweebi | Seed | USD 500,000 | Inflection Point Ventures and others |

Konstella | Series A | USD 3.0 million | ADATA Technology |

Turing Dream | Series A | EUR 2.0 million, about USD 2.2 million to USD 2.3 million | SETT / Spanish Society for Technological Transformation |

Chalkie | Series A / Funding round | USD 4.0 million | TriplePoint Ventures |

GAGA | Seed / Pre-Series A | USD 2.5 million | Phoenix Venture Partners |

Drivers Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Rising demand for online learning | +4.2% | Global, North America, Asia Pacific | Supports wider digital learning adoption. |

Growth in smart classrooms | +2.8% | North America, Europe, China, India, GCC | Increases demand for digital classroom tools. |

Adoption of AI-based learning | +3.5% | U.S., Canada, UK, China, India, South Korea | Improves personalized and adaptive learning. |

Expansion of mobile learning | +2.6% | Asia Pacific, Latin America, Middle East & Africa | Expands access through smartphones and tablets. |

Rising demand for skill-based education | +3.1% | U.S., Europe, India, Southeast Asia | Supports online certification and career learning. |

Restraints Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

High implementation cost | -2.1% | Emerging markets, small institutions, rural areas | Limits adoption by price-sensitive users. |

Limited internet access | -1.8% | Rural Asia Pacific, Africa, Latin America | Restricts online learning reach. |

Data privacy concerns | -1.3% | North America, Europe, developed Asian markets | Raises compliance and trust challenges. |

Resistance to digital adoption | -1.0% | Traditional institutions, rural education systems | Slows platform adoption. |

Unequal access to digital devices | -1.6% | Asia Pacific, Africa, Latin America | Widens the digital learning gap. |

Opportunities Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

Growth in personalized learning | +3.4% | North America, Europe, Asia Pacific | Creates demand for learner-specific platforms. |

Expansion of corporate training | +3.0% | U.S., Europe, India, Southeast Asia | Supports workforce upskilling demand. |

Rising investment in digital education | +2.7% | U.S., China, India, GCC, Southeast Asia | Encourages platform and product expansion. |

Increasing adoption in emerging markets | +3.2% | India, Indonesia, Brazil, Africa, Middle East | Opens new growth areas. |

Growth of online degree programs | +2.4% | North America, Europe, Asia Pacific | Expands higher education access. |

Segment Insights

By Sector Analysis

In 2025, K-12 leads the EdTech market with around 59.1% share, supported by the wide use of digital classrooms, learning management systems, smart boards, and online assessment tools in schools. The segment is strongly linked with public and private school digitalisation, where technology is being used to improve access, classroom delivery, student tracking, and learning support. UNESCO notes that digital technology has changed education delivery, although its value depends on proper access, teacher readiness, and suitable use in classrooms.

The demand from K-12 institutions is also being supported by the need for hybrid learning, personalised content, and better parent-teacher-student engagement. In the U.S., 96% of public schools reported providing digital devices to students who needed them by the beginning of the 2021-22 school year, showing the strong role of school-level device access in EdTech adoption.

By Type Analysis

In 2025, Hardware accounts for 41.9% of the EdTech market, as schools, colleges, and training centres continue to invest in tablets, laptops, interactive displays, projectors, servers, and classroom connectivity tools. The segment remains important because digital learning cannot scale effectively without physical infrastructure, especially in classrooms where blended learning and computer-based testing are increasing.

The growth of hardware demand can also be linked to the need for reliable device access among learners and teachers. OECD has stated that access to digital tools and resources is essential for education, but it must be supported by age-appropriate guidance and effective classroom management. This supports steady investment in devices, while also keeping attention on responsible and outcome-based use.

By Deployment Mode Analysis

In 2025, On-premise solutions dominate the EdTech market with 72.3% share, mainly because many schools, universities, and government education systems prefer direct control over data, content, system access, and internal IT operations. This model is often selected where student data privacy, examination security, institutional compliance, and local network control are important.

The preference for on-premise deployment is also stronger in institutions with established IT teams and existing campus infrastructure. At the same time, digital education systems are increasingly being used for data-driven decision-making, early warning systems, and learning management, which makes secure deployment architecture an important buying factor for education providers.

By End-User Analysis

In 2025, Individual learners lead the market with around 47.8% share, supported by rising demand for self-paced learning, online tutoring, professional upskilling, exam preparation, and mobile-based learning. This segment is expanding because learners are increasingly using digital platforms to gain flexible access to courses, certificates, language learning, coding, and job-oriented skills.

The adoption is also being supported by the need for lifelong learning and workforce readiness. The World Bank highlights that digital platforms can improve access, relevance, and quality in technical education and workforce training, especially as young people require stronger digital and foundational skills for employment.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFBy Regional Analysis

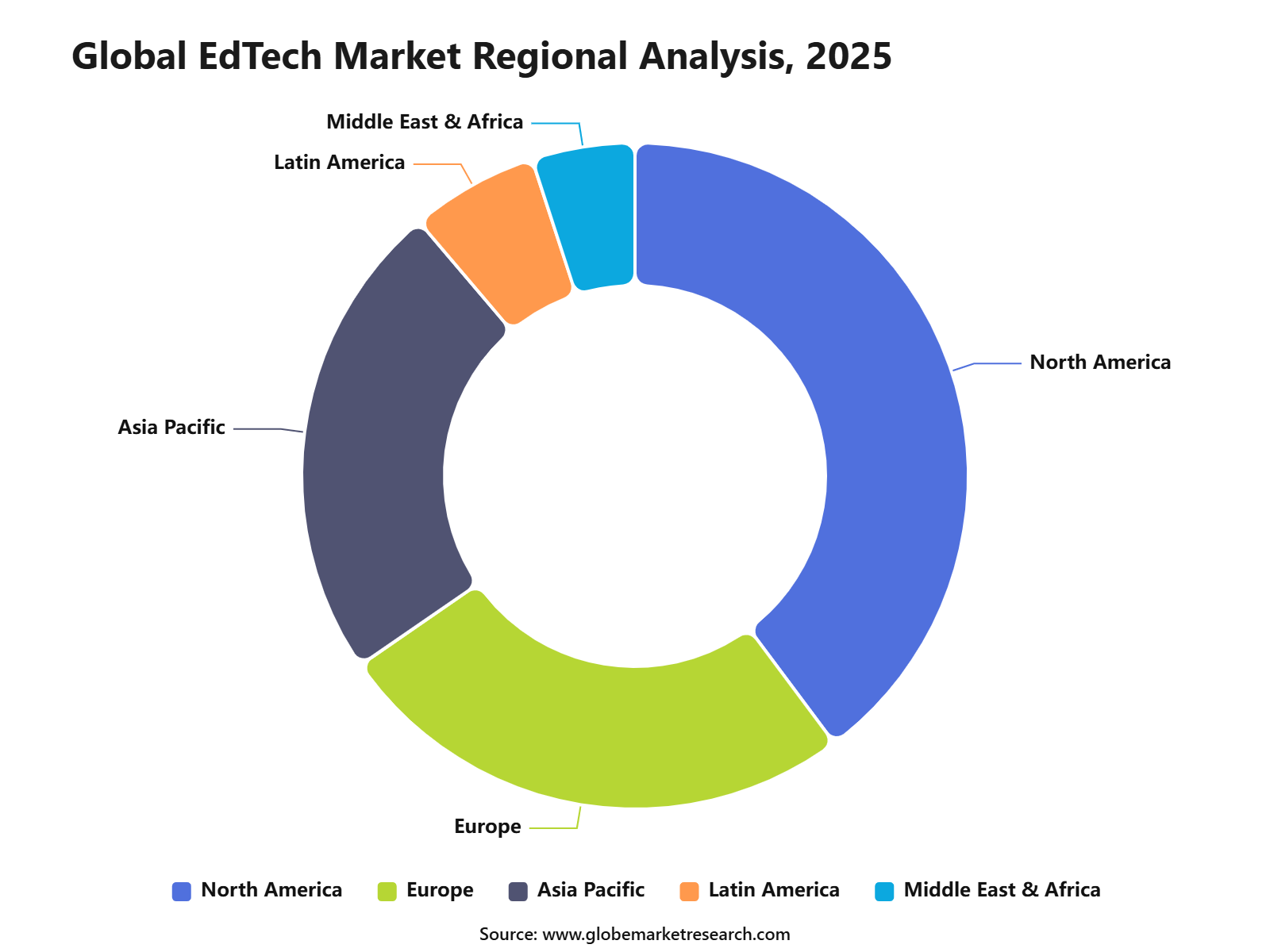

In 2025, North America holds a leading regional position with 39.8% share, supported by high digital infrastructure, strong school technology spending, wide internet access, and early adoption of online learning platforms. The U.S. remains a key contributor, with a stated value of USD 53.9 Bn and a 15.6% CAGR, supported by continued use of digital tools across K-12, higher education, and professional learning.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFThe region’s strength is also supported by strong household connectivity and school-level technology access. In the U.S., 97% of children aged 3 to 18 had home internet access in 2021, while 93% had access through a computer, creating a strong base for online and blended education models.

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDF

iThe graph shows projected market growth until 2035 based on CAGR analysis. Actual outcomes may vary depending on changing demand, competition, and economic factors.To gain greater insights - request a sample report PDFRegional Impact Analysis

Impact Factor | Estimated CAGR Impact | Regional Relevance | Market Impact |

|---|---|---|---|

North America market leadership | +4.0% | U.S. and Canada | Maintains strong adoption base. |

Europe digital education adoption | +2.8% | UK, Germany, France, Nordic countries | Supported by policy and institutional use. |

Asia Pacific growth expansion | +4.5% | China, India, Japan, South Korea, Southeast Asia | Driven by large student population. |

Latin America digital learning demand | +2.4% | Brazil, Mexico, Chile, Colombia | Supported by improving connectivity. |

Middle East and Africa education digitization | +2.2% | UAE, Saudi Arabia, South Africa, Egypt | Driven by education modernization programs. |

Key Market Segments

Deployment Mode

Cloud

On-Premise

Type

Hardware

Software

Content

Sector

K-12

Preschool

Higher Education

Other Sectors

End-User

Individual Learners

Institutes

Enterprises

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Top Emerging Trends

Artificial intelligence is becoming a major trend in the EdTech market as learning platforms increasingly use AI for personalized lessons, automated feedback, content support, and student performance tracking. In 2024, 37% of lower secondary teachers reported using AI in their work, while 57% agreed that AI helps them write or improve lesson plans, showing rising acceptance of AI-supported teaching tools.

Cloud-based learning platforms are also gaining strong adoption because they support online classes, digital content, student records, assessments, and teacher-student communication from one system. This trend is supported by the global digital learning gap, as nearly 1.3 billion school-age children still do not have internet access at home, which creates demand for scalable, low-cost, and mobile-friendly education platforms.

Skill-based and employment-linked learning is becoming more important as students and workers seek job-ready training, certifications, coding skills, language learning, and professional development. This trend is supported by the global skills mismatch, which has increased the need for flexible learning platforms that can support reskilling and lifelong learning across schools, universities, and workplaces.

Growth Factors

The growth of the EdTech market can be attributed to the rising demand for flexible and accessible learning models across schools, higher education, and corporate training. Online and hybrid learning have become widely used because they allow learners to study beyond physical classrooms, support self-paced education, and help institutions reach students across wider locations.

A key growth factor is the need to improve learning outcomes, especially in developing economies. The World Bank reported that over half of 10-year-olds in low- and middle-income countries cannot read and understand an age-appropriate text, which supports demand for adaptive learning tools, digital assessments, foundational learning platforms, and teacher support systems.

Rising digital access is also supporting EdTech adoption, although the opportunity remains uneven across regions. Around two-thirds of school-age children, equal to nearly 1.3 billion children globally, do not have internet access at home, which creates strong demand for offline-enabled learning, mobile-first platforms, public digital education programs, and low-bandwidth education solutions.

Government focus on digital education is further strengthening market expansion. In 2024, around 251 million children and young people were out of school, while 468 million lived in conflict zones as of 2023, which shows the need for remote learning tools, digital content delivery, education continuity platforms, and inclusive learning solutions.

Recent Developments

May 2026 – Coursera announced a merger with Udemy in a deal valued at nearly USD 2.1 billion to strengthen AI-driven workforce learning and certification services.

April 2026 – Blackboard launched advanced AI and immersive learning solutions after investing around USD 120 million in product innovation and digital learning upgrades.

July 2025 – Pearson acquired eDynamic Learning in a transaction estimated at USD 210 million to expand career and technical education offerings.

March 2025 – Microsoft expanded Copilot AI integration across education platforms with investments exceeding USD 300 million in AI-powered classroom productivity tools.

February 2025 – Google for Education launched AI-enabled Chromebook and classroom tools as part of a broader education technology investment program valued at nearly USD 250 million .

January 2025 – Samsung Electronics introduced upgraded smart classroom displays and connected education systems supported by approximately USD 180 million in R&D spending.

Report Scope

Report Highlights | Details |

|---|---|

Market Revenue (2025) | USD 279.8 Bn |

Forecast Revenue (2035) | USD 1,255.8 Bn |

CAGR (2025-2035) | 13.9% |

Base Year for Estimation | 2025 |

Historic Data | 2020-2024 |

Forecast Period | 2025-2035 |

Report Coverage | AI impact analysis, Revenue projections, company positioning, competitive analysis, growth drivers, and emerging market trends |

Segments Covered | By Sector (Preschool, K-12, Higher Education and Other Sectors), By Type (Hardware, Software and Content), By Deployment Mode (Cloud-based and On-premises), By End-User (Individual Learners, Institutes and Enterprises), By Regional Insights, Adoption Trends, Leading Companies |

Regional Analysis | Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; North America – US, Canada; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

Key companies profiled | Pearson, Blackboard, Microsoft, Google for Education, Apple, Coursera, Khan Academy, Adobe, Moodle, Instructure, Samsung Electronics, SMART Technologies, Udemy, Dell Technologies, Cisco Systems, Intel Corporation, Lenovo, Epic Systems, Descartes Systems, Seesaw Learning and Others |

Customization Scope | Tailored insights for specific regions, countries, and market segments can be provided. Additional report customization is available upon request. |

Competitive Landscape

The market is characterized by intense competition among established players and emerging companies. Strategic partnerships, mergers and acquisitions, and product innovation are key strategies employed by market participants.

Key Market Players

Coursera Inc.

BYJU’S

Chegg Inc.

Pearson

Khan Academy

Coursera

Meet the Team

This report was prepared by our expert analysts with deep industry knowledge and research experience.

Kevin is a market research analyst with expertise in industry analysis, market sizing, competitive benchmarking, and growth opportunity assessment. Her work focuses on delivering clear, data-backed insights that help businesses understand market trends, customer demand, emerging technologies, and investment potential across global industries.

I am a market research professional with over 7 years of experience delivering data-driven insights that support strategic decision-making. I hold a BSc in Biotechnology and an MBA in Marketing, allowing me to effectively bridge scientific understanding with business strategy. My expertise lies in analyzing complex healthcare trends, market dynamics, and competitive landscapes to help organizations identify opportunities and navigate evolving industry challenges. I am passionate about transforming research into actionable insights that drive informed growth and innovation in the sector.

Frequently Asked Questions

Related Reports

More in Information and Technology

Voice AI Agents Market to Hit USD 113.7 Billion by 2035

Global Voice AI Agents Market Size, Share Analysis Report By Solution (Voice AI Platform, Services (Professional Services(Implementation & Integration, Consulting & Training Services, Support and Maintenance Services), Managed Services)), By Deployment (Cloud Based, On Premises), By Enterprise Size (Small & Medium Enterprise Size, Large Enterprises), By Industry (BFSI, Automotive, Healthcare, Retail & E-commerce, IT & Telecom, Aerospace & Defence, Others (Utilities, Media & Entertainment)), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

AI Trust, Risk and Security Management (AI TRiSM) Market to hit USD 39.8 Bn by 2026

Global AI Trust, Risk and Security Management (AI TRiSM) Market Size, Share Analysis Report By Component (Solutions, Services), By Technology (ML based TRiSM, Natural Language Processing based TRiSM, Explainable AI (XAI), Federated Learning/Privacy-Preserving ML), By Application (Model Governance & Compliance, Model Monitoring & Observability, Data Privacy & Security, Bias Detection & Mitigation, Identity & Access Security for AI), By Deployment (On-premises, Cloud), By Organization Size (Large Enterprises, Small & Medium Enterprises), By Industry Vertical (BFSI, Healthcare, Retail & E-commerce, IT & Telecom, Government & Defense, Manufacturing, Transportation & Logistics), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

K-12 Education Technology (EdTech) Market to hit USD 491.5 Bn by 2035

Global K-12 Education Technology (EdTech) Market Size, Share Analysis Report By Component (Hardware, Software, Services), By Deployment Mode (Cloud-Based, On-Premises), By Technology Type (Learning Management Systems (LMS), Student Information Systems (SIS), Gamification & Game-based Learning, AR/VR in Education, AI-enabled Learning Tools, Adaptive & Personalized Learning, eContent & Digital Courseware), By Application (Classroom Learning, Remote Learning / Online Learning, Curriculum Management, Content Delivery & Digital Textbooks and Others), By End User (Public K-12 Schools, Private K-12 Schools, Charter Schools, Home Schools), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035

US Esports Market to hit USD 29.3 Bn by 2035

US Esports Market Size, Share Analysis Report By Revenue Source (Advertising & Sponsorships, Media Rights, Merchandise & Tickets, Others), By Platform (PC Gaming Platforms, Console Gaming Platforms, Mobile & Tablet Platforms, Others), By Game Genre (MOBA Games, First-Person Shooter Games, Battle Royale Games, and Others), By Streaming Type (Live Streaming, On-Demand Streaming, Hybrid Streaming), By Device Type (Smartphones, PC, Console, Others), By End User (Advertisers & Sponsors, Game Publishers, Streaming Platforms, Tournament Organizers, Teams & Players, Viewers/Fans), By Regional Insights, Business plan and Project Report, Investment Opportunities, Profitability, Industry Trends, Leading Companies and Growth Forecasts by 2025-2035